What is NCUA’s Authority to Use the Hammer of Safety and Soundness?

- Feb 14, 2021

- 4 min read

Updated: Feb 17, 2021

What is NCUA’s Authority to Use the hammer of Safety and Soundness?

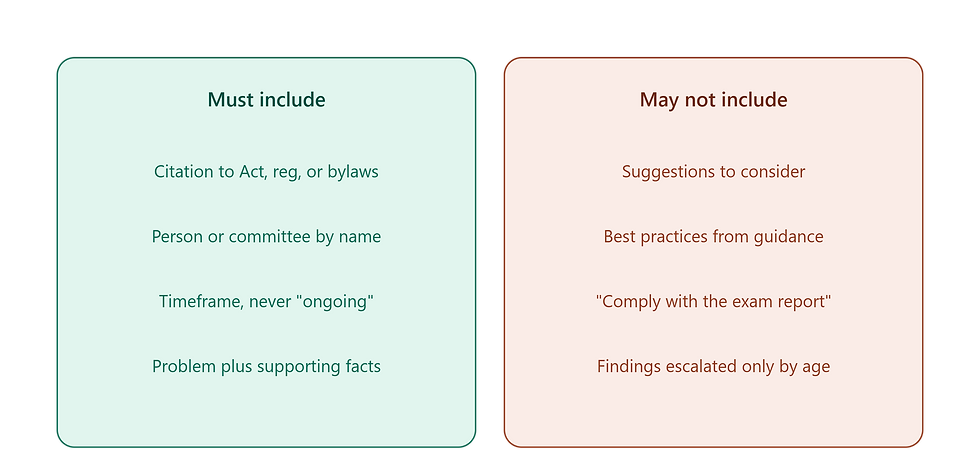

The examiner wants to discuss the need for a Document of Resolution.

You want to know what regulation or law you have violated?

The examiner cites “safety and soundness.”

You still ask for a connection to a regulation or law.

The examiner or supervisory examiner refer you to NCUA's regulations Section 741.3, which, in part, requires credit unions to operate in a safe and sound manner as a condition of insurance.

An astute NCUA staffer may even cite the NCUA Supervision Policy Manual which states:

"Section 206(b)(1)of the Federal Credit Union Act gives the NCUA the ability to terminate insurance for unsafe and unsound practices. Even though a DOR may not lead to termination of insurance, the Act implies credit unions must operate in a safe and sound manner as a condition of insurance."

So the act implies the requirement to operate safe and sound, then NCUA issues a regulation based on that implication that requires safe and sound operations – still with me?

Then the examiner indicates that the safety and soundness issue requires you to comply with NCUA guidance such as a letter to credit unions.

So you say I noticed the NCUA Board recently approved Interagency Statement Clarifying the Role of Supervisory Guidance. In defense of your position you cite a quote of then Chairman Rodney Hood:

“The 2018 interagency statement reiterated well-established law by stating that, unlike a law or regulation, supervisory guidance does not have the force and effect of law. As a result, supervisory guidance does not create binding legal obligations for the public. The proposed rule is intended to confirm that agencies will continue to follow and respect the limits of administrative law in carrying out their supervisory responsibilities.”

Then you cite the interagency statement directly:

Difference between supervisory guidance and laws or regulations

“A law or regulation has the force and effect of law.1 Unlike a law or regulation, supervisory guidance does not have the force and effect of law, and the agencies do not take enforcement actions based on supervisory guidance. Rather, supervisory guidance outlines the agencies’ supervisory expectations or priorities and articulates the agencies’ general views regarding appropriate practices for a given subject area. Supervisory guidance often provides examples of practices that the agencies generally consider consistent with safety-and-soundness standards or other applicable laws and regulations, including those designed to protect consumers. Supervised institutions at times request supervisory guidance, and such guidance is important to provide insight to industry, as well as supervisory staff, in a transparent way that helps to ensure consistency in the supervisory approach.”

The examiner says well that doesn’t say we cannot use guidance in a DOR (which is an informal enforcement action)– and now you are really perplexed because you think it means exactly that, yet not wanting to tick off your examiner.

What gives?

So NCUA agrees that guidance does not have the force of law and won’t take enforcement actions based on it, yet NCUA cites safety and soundness in the DOR, with the link being the safety and soundness regulation derived from an implied reference to operating safe and sound… then the NCUA examiner puts Language in the DOR requiring compliance with the guidance which is not law or regulation!

Here is how they get away with it:

the paragraph below is also from the guidance and provides an exception for using guidance in writing (in the examination and thus in the DOR)

“Examiners will not criticize a supervised financial institution for a “violation” of supervisory guidance. Rather, any citations will be for violations of law, regulation, or non-compliance with enforcement orders or other enforceable conditions. During examinations and other supervisory activities, examiners may identify unsafe or unsound practices or other deficiencies in risk management, including compliance risk management, or other areas that do not constitute violations of law or regulation. In some situations, examiners may reference (including in writing) supervisory guidance to provide examples of safe and sound conduct, appropriate consumer protection and risk management practices, and other actions for addressing compliance with laws or regulations.”

It is this last underlined sentence which would allow an examiner to put safety and soundness best practices as identified via guidance, and the link that to the regulation, which makes it a violation of law and enforceable. Got it?

In NCUA’s defense safety and soundness is the heart and soul of the financial system and I don’t mean to make light of it, rather to explain that there is a fine art to understanding NCUA.

I understand your frustration as a CEO, trying to meet your fiduciary responsibilities and having to dance the dance of safety and soundness described above. I help my clients dance the dance with NCUA. I understand NCUA inside and out. Let me assist you during your examination saving you time and money.

If you would like to talk about possibly adding my experience to your team email me at info@marktreichel.com , or schedule your FREE strategy session by clicking HERE

Comments