What Is a Prohibition?

- Feb 9

- 4 min read

What Is a Prohibition?

A prohibition action is one of the National Credit Union Administration’s most severe enforcement tools. While it is often discussed alongside removal actions, prohibition is broader in scope and longer-lasting.

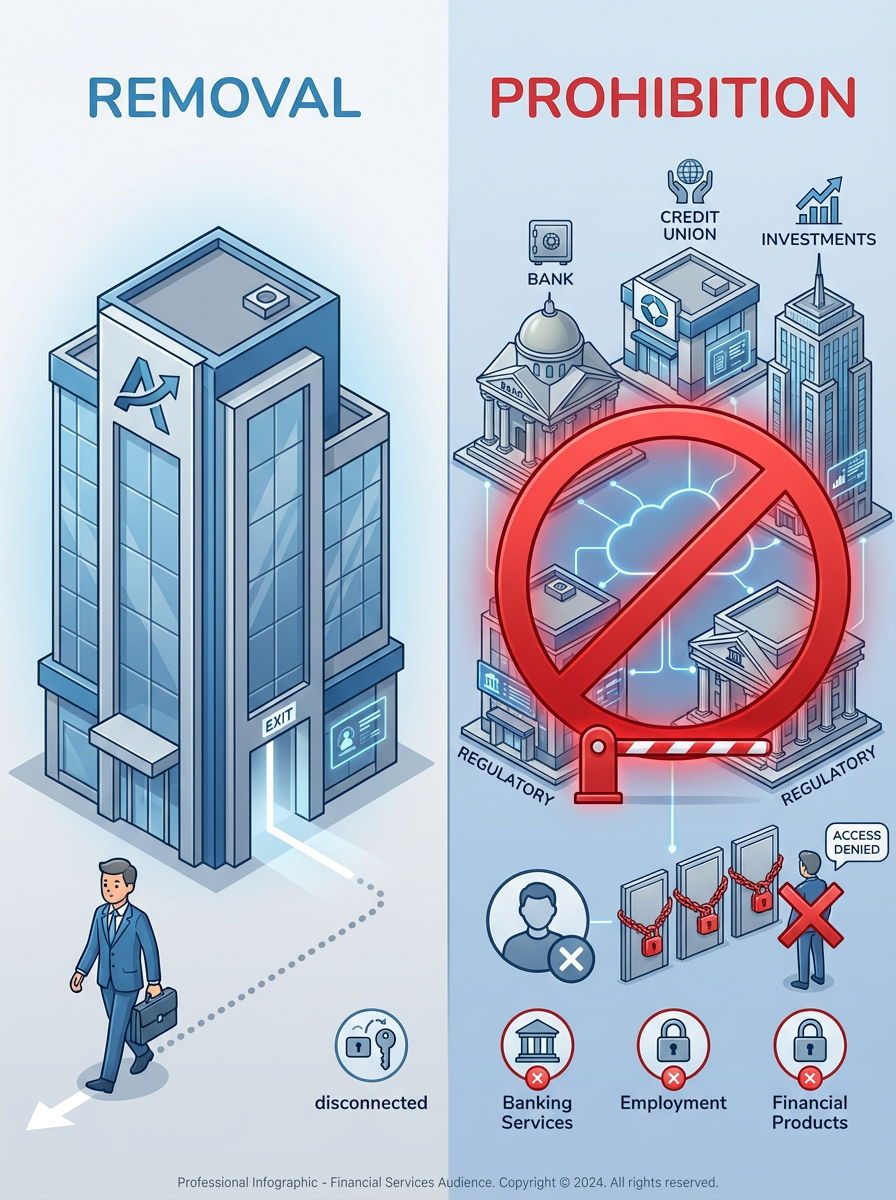

A removal action strips an individual of a specific role — such as director, officer, or committee member — at a particular credit union. A prohibition, by contrast, bars an individual entirely from participating in the affairs of any federally insured financial institution.

This distinction matters because not all institution-affiliated parties are elected or appointed officials. Consultants, contractors, agents, and other third parties may fall outside the scope of removal authority. In those cases, National Credit Union Administration uses prohibition to permanently cut off further involvement with the credit union system.

NCUA’s authority to issue prohibition orders comes from Section 206(g) of the Federal Credit Union Act, and the procedural rules governing prohibition hearings are found in NCUA Rules and Regulations, Part 747, Subpart A.

How Prohibition Differs from Other Enforcement Actions

Like removal actions, prohibition is not anticipatory. It is not designed to prevent potential future misconduct in the way a cease-and-desist order is. Instead, prohibition follows a completed enforcement process.

NCUA may issue a prohibition only after:

Serving a Notice of Intent to Prohibit and completing the applicable administrative proceedings, or

Receiving the institution-affiliated party’s consent.

Where appropriate, NCUA may combine removal and prohibition proceedings into a single action. Procedurally, the mechanics of a prohibition case largely mirror those used in removal cases.

Importantly, prohibition authority does not disappear simply because the individual resigns or is terminated. NCUA may pursue a prohibition action even after the individual has left the credit union, including situations involving liquidation or other termination of the relationship.

Under the statute, NCUA has up to six years after resignation, termination, liquidation, or separation to bring a prohibition action.

Immediate Prohibition Orders

In certain circumstances, NCUA may issue an immediate prohibition order to protect the credit union or its members.

The legal standard for immediate prohibition is the same as that used for an immediate suspension of an official. Where immediate action is warranted, the prohibition becomes effective at once, without waiting for the conclusion of standard administrative proceedings.

Grounds for Prohibition

The grounds for prohibition are the same as those for removal. In practice, this typically involves findings related to misconduct, breaches of fiduciary duty, unsafe or unsound practices, or actions that result in financial loss or damage to the credit union or its members.

Mechanics of a Prohibition Action

A prohibition case typically begins at the examination level. The examiner prepares a formal recommendation that includes:

Identification of the individual subject to prohibition, including name, business address, position, and relationship to the credit union or related enterprise

Sufficient evidence to establish the legal grounds for prohibition

Specific details regarding the conduct at issue, including events that caused or could cause financial loss, damage, or improper personal benefit

Once NCUA determines that grounds exist, the Office of General Counsel serves a Notice of Intent to Prohibit on the individual.

The notice outlines the hearing process. Hearings are generally scheduled no sooner than 30 days and no later than 60 days after service of the notice.

Prohibition Involving Felonies

Special procedures apply when prohibition or removal involves a felony offense.

NCUA may pursue immediate suspension or prohibition when an institution-affiliated party meets all of the following criteria:

Is charged with a crime involving dishonesty or breach of trust

Faces a potential penalty of more than one year of imprisonment under federal or state law

Poses a threat to the credit union’s members or risks undermining public confidence

Examiners must develop tangible evidence supporting the action. Examples include:

Member meetings seeking resignation or removal

Share outflows

Membership cancellations tied to dissatisfaction with continued service

Significant adverse publicity

Difficulty obtaining funding from regular sources

Examiners are instructed not to express opinions regarding guilt or innocence. The administrative action remains in place until the criminal matter is resolved or NCUA terminates the proceeding.

Outcomes After Criminal Proceedings

If the individual is convicted and the judgment is final (or if the individual enters a pretrial diversion or similar program), NCUA may issue a final order of removal or prohibition.

An acquittal does not automatically prevent NCUA from proceeding under its general removal or prohibition authority. In those cases, NCUA must rely on the standard enforcement provisions rather than the felony-specific authority.

Felony Prohibition Procedure at a Glance

In felony-based cases, the administrative process follows a distinct path:

The NCUA Board issues a Notice of Suspension and/or Prohibition, effective immediately

No hearing is held unless the individual requests one in writing within 30 days

If requested, an informal hearing is held in Washington, D.C. — not before an administrative law judge

Upon final conviction, the Board may issue a final order of removal or prohibition

If acquitted, NCUA may still proceed under general statutory authority

The presiding officer submits a recommended decision to the Board within 10 days

The Board issues its final decision within 60 days

Bottom Line

Prohibition is the regulatory equivalent of a lifetime ban from the federally insured financial system. It reaches beyond titles, boards, and employment status — and it can follow individuals long after their formal relationship with a credit union has ended.

For institution-affiliated parties, prohibition represents the most consequential enforcement action NCUA can take. For credit unions, it underscores the importance of early governance intervention, documentation, and escalation when serious issues surface.

Comments