Q4 Credit Union Data: Looks Good… But Worth a Closer Look

- Mar 17

- 2 min read

We went through the Q4 credit union data on this week’s With Flying Colors podcast.

At a high level, things look good. Capital is strong. Earnings held up. Liquidity improved. Nothing jumping off the page as a problem.

But when you spend a little time with the numbers, a few things start to stand out.

2025 Was Kind of a Reset Year

After everything the industry went through—COVID deposits, inflation, rate hikes—2025 felt like a year to catch your breath.

Margins improved. Funding pressures eased a bit. Balance sheets look cleaner than they did a couple years ago.

That’s all good.

But it also feels like we’re at a transition point.

A Few Trends Worth Watching

Nothing here is a five-alarm fire, but these are the things that caught my attention:

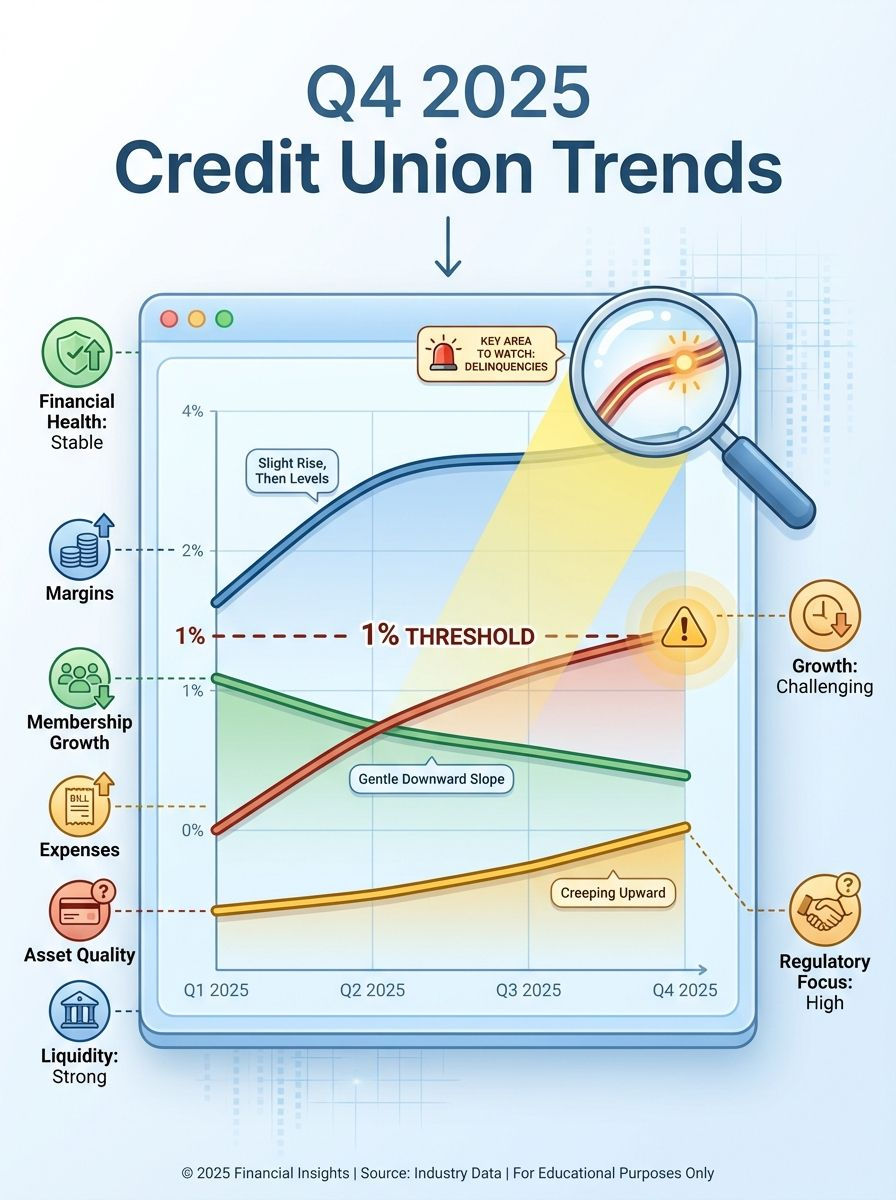

Delinquency is now over 1%. First time we’ve seen that in about a decade. Still manageable, but it’s moved.

Membership growth slowed to around 2%. That raises a longer-term question about where new members are coming from.

Expenses keep going up. Wages, technology, everything it takes to stay competitive—it’s all getting more expensive.

Margins may have topped out. The lift from higher loan yields looks like it’s starting to level off.

Individually, none of these are a big deal. But they’re all moving in the same direction.

If There’s One Thing to Watch

For me, it’s asset quality.

That’s usually where issues show up first.

We’re starting to see some movement—real estate in particular, and some pockets of commercial lending. It’s not widespread, but it’s there.

And once that starts to move, it tends to ripple through everything else.

Big Picture

The industry is still in a good spot. No question about that.

But this feels like one of those moments where things can shift quietly before they show up in a big way.

The numbers still look good.

The question is what they look like a year from now.

Comments